Traditional Medicare vs. Medicare Advantage

NOTE: Health, fitness, finances, etc. are concerns for those of the Sage age. Periodically, we will provide information about these "real-world" challenges. Never see what we provide as the sum of the conversation. - Carlton L Coon, Sr.

Traditional Medicare is a government-funded medical insurance option for people age 65 and older. Many older Americans use Medicare as their primary insurance since it covers:

Inpatient hospital services (Medicare Part A). These benefits include coverage for hospital visits, hospice care, and limited skilled nursing facility care and at-home health care.

Outpatient medical services (Medicare Part B). These benefits include coverage for preventive, diagnostic, and treatment services for health conditions.

Traditional Medicare generally doesn’t cover prescription drugs, dental, vision or hearing services, or additional healthcare needs. However, for people who have enrolled in traditional Medicare, there are add-ons such as Medicare Part D prescription drug coverage and Medicare supplement (Medigap) plans that can offer additional coverage.

Traditional Medicare costs:

How does Medicare Advantage work?

Medicare Advantage (Part C) is an insurance option for people who are already enrolled in Medicare Part A and Part B.

Medicare Advantage plans are offered through private insurance companies, and many plans cover hospital, medical insurance, and additional services such as:

fitness services, plus other health perks

Medicare Advantage takes the place of Traditional Medicare add-ons, such as Part D and Medigap. Instead of having multiple insurance plans to cover medical costs, a Medicare Advantage plan offers all your coverage in one place.

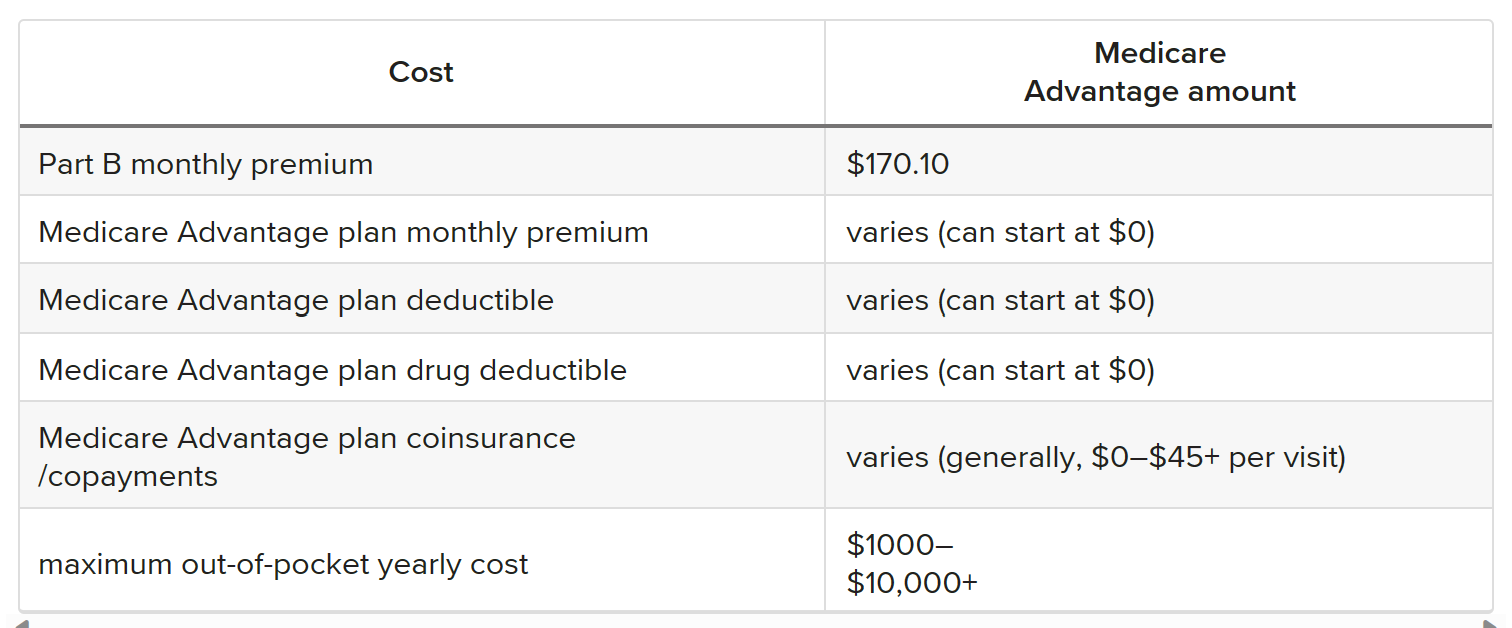

Medicare Advantage Costs:

What to consider when choosing between Medicare vs. Medicare Advantage

Traditional Medicare and Medicare Advantage differ in their coverage, costs, and benefits. When comparing your options, there’s no “one plan fits all.”

Medical services

If you’re someone who rarely visits the doctor, Medicare and Medicare add-ons may cover most of your needs.However, if you’re someone who wants coverage for yearly dental, vision, or hearing exams, many Medicare Advantage plans offer this type of coverage.

Health conditions

If you have a chronic health condition, such as cancer, chronic heart failure, stroke, dementia, or others, it’ll affect your medical coverage. For example, Medicare may not cover all your needs, but a Medicare Advantage Special Needs Plan (SNP) could help with long-term costs.

These plans are designed for people with one of several chronic health conditions. They offer:

coverage for specialists and case managers

access to medications specifically for your condition

access to other benefits

ResearchTrusted Source has shown that Medicare Advantage plans can help consumers save more money on certain medical necessities, such as laboratory tests and medical equipment.

Medications

Traditional Medicare generally doesn’t cover prescription drug costs. To receive coverage for prescription drugs, you need a Medicare Part D plan or Medicare Advantage plan with prescription drug coverage. No matter what option you choose, you’re required to have some form of prescription drug coverage within 63 days of enrolling in Medicare, or you’ll be required to pay a permanent late enrollment penalty.

Budget

If you have Medicare, you’ll pay a monthly premium for Part A (if you don’t qualify for premium-free Part A) and Part B, yearly deductibles for parts A and B, and other costs if you buy add-on coverage. If you have Medicare Advantage, you may need to pay additional costs as well, depending on the plan you choose. Before deciding on the type of Medicare plan you want, consider what out-of-pocket costs you can afford each year.

Provider preference

While Medicare offers the freedom to choose any provider within the Medicare network, most Medicare Advantage plans don’t provide as much freedom. Depending on the type of Medicare Advantage plan you have, you may face additional costs for out-of-network services, as well as specialist referrals and visits.

Travel frequency

For some people, travel is a way of life. This is especially true for people who retire and choose to travel or who live someplace warmer during the colder months. If you travel frequently, consider what out-of-state medical needs you may have. In most cases, Medicare coverage is nationwide, while Medicare Advantage plans require you to stay in your local area for medical services.

Source: Medicare vs. Medicare Advantage: What's the Difference? (healthline.com)

**UPCI Sages is not an officlal representative of Traditional Medicare or Medicare Advantage. For official guidance, refer to www.medicare.gov.